hotelvak.eu

EN

Platform on hotelmanagement, interiordesign and design in the Netherlands

For the first time in over ten years, the number of overnight stays in the Netherlands is falling. This suggests that 2026 is set to be a turning point for the accommodation sector. Since 1 January, accommodation providers – with the exception of campsites – have been subject to a VAT increase from 9 to 21 per cent. Initial figures show that the market is reacting immediately to this: in the first four months of 2026, the number of overnight stays fell across the board. Foreign guests, in particular, are staying away more often. What does this reversal in the trend mean for hotels, holiday parks and other accommodation providers?

Differences within the sector are growing. Fast food performed well in the first quarter, whilst hotels showed hardly any growth. At the same time, the number of overnight stays in the Netherlands is falling and concerns about price trends are mounting. The rise in procurement costs is expected to become more apparent in the fourth quarter of 2026. In addition, the minimum youth wage will rise in 2027, which may further increase costs for businesses. Despite the rise in purchasing power, consumption is lagging behind. This is having a downward effect on the sector. This picture is consistent with in our previously published sector forecasts.

Restaurant turnover rose by 1.6 per cent in the first quarter. This growth is entirely due to higher prices. Volumes, on the other hand, are showing a downward trend, particularly in March. This is mainly because March 2025 was a relatively strong month due to favourable weather conditions compared with March 2026.

Unlike in previous years, the fast-food sector is showing a clear improvement. The sub-sector recorded revenue growth of 3.8 per cent in the first quarter, thereby outperforming the hospitality sector as a whole. The recovery following previous difficult years therefore appears to be continuing. However, inflation remains a risk, as higher prices could once again put pressure on volumes.

Cafés are showing a stable performance compared with 2025. Turnover rose slightly, by 1.3 per cent, in the first quarter. Here too, the growth is mainly due to price rises. Volumes remain under pressure.

Turnover in the hotel sector rose by 0.4 per cent in the first quarter. This growth was mainly driven by January, when accommodation saw relatively strong growth. Snow caused a temporary surge in demand at that time, particularly in the Schiphol region, due to delayed and cancelled flights. However, over the first four months of 2026, the number of overnight stays in the Netherlands has fallen.

The first quarter of 2026 looked reasonably good for campsites and holiday parks, with turnover growth of almost 5.5 per cent. This growth was largely due to price rises. From April onwards, the market became more challenging. Both hotels and other accommodation providers saw the number of overnight stays fall.

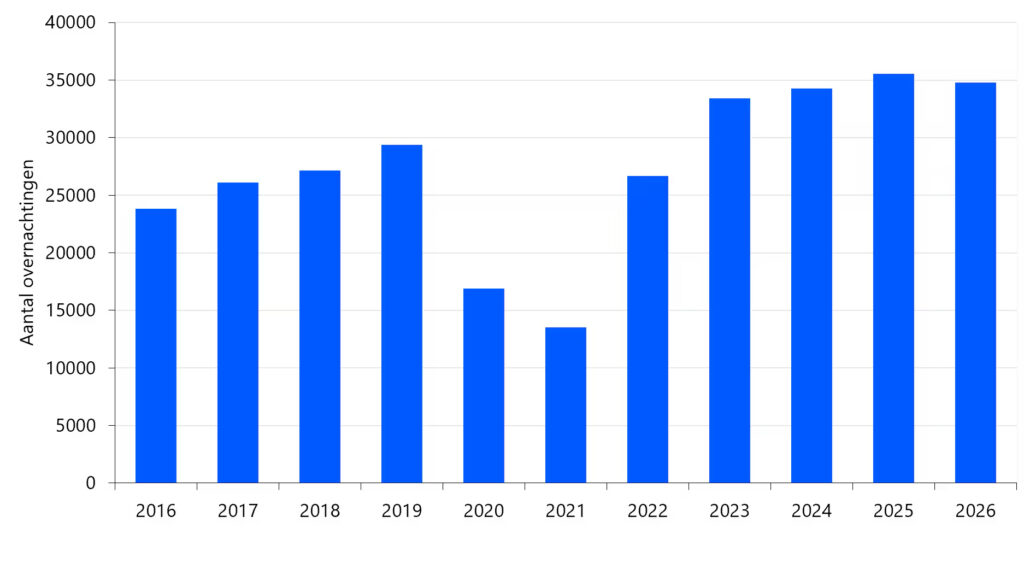

The number of overnight stays in the Netherlands has grown almost continuously over the past 10 years. There has been steady growth since 2013. Only in 2020, 2021 and 2022 did the number of overnight stays fall due to COVID-19 measures. This growth is in line with the global trend of a rapidly expanding tourism sector. Between 2013 and 2025, the number of overnight stays from January to April rose by over 75 per cent.

Figure 1:

Trend in the number of overnight stays up to and including April.

In 2026, we see the first break in the trend, with a decline in the number of overnight stays in the first four months of the year. Although these months do not account for the bulk of overnight stays, this is nevertheless typical of the market situation. The number of overnight stays fell by 2.2 per cent in the first four months.

The number of overnight stays by both domestic and international guests fell. In recent years, international guests had actually been the driving force behind growth. Now, they are staying away more often. The number of overnight stays by international guests fell by 567,000, a drop of 3.2 per cent. The number of overnight stays by domestic guests fell by 217,000, a decrease of 1.1 per cent.

What is striking is that visitors from our neighbouring countries, in particular, visited the Netherlands less frequently. Germany and Belgium are traditionally important source markets for the Dutch accommodation sector. The number of overnight stays by German guests fell by 5.1 per cent and that of Belgian guests by 4.9 per cent. Together, they accounted for 407,000 fewer overnight stays in our country. It is striking that, in the first three months, more German guests actually visited the Netherlands. The decline in April completely reversed this trend.

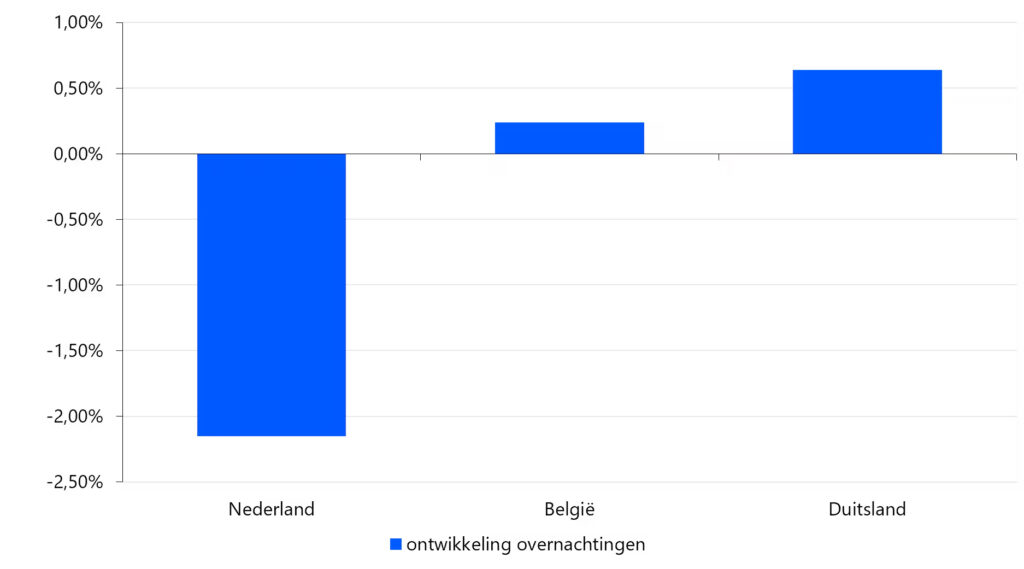

The number of overnight stays in the Netherlands fell by 2.2 per cent in the first quarter. In Belgium and Germany, the number of overnight stays rose slightly, by 0.24 per cent and 0.64 per cent respectively. Growth in our neighbouring countries is therefore limited, but the difference compared with the Netherlands is striking. The VAT increase appears to be having an impact in this way.

Figure 2:

Trend in overnight stays in the first quarter of 2026 compared with the first quarter of 2025.

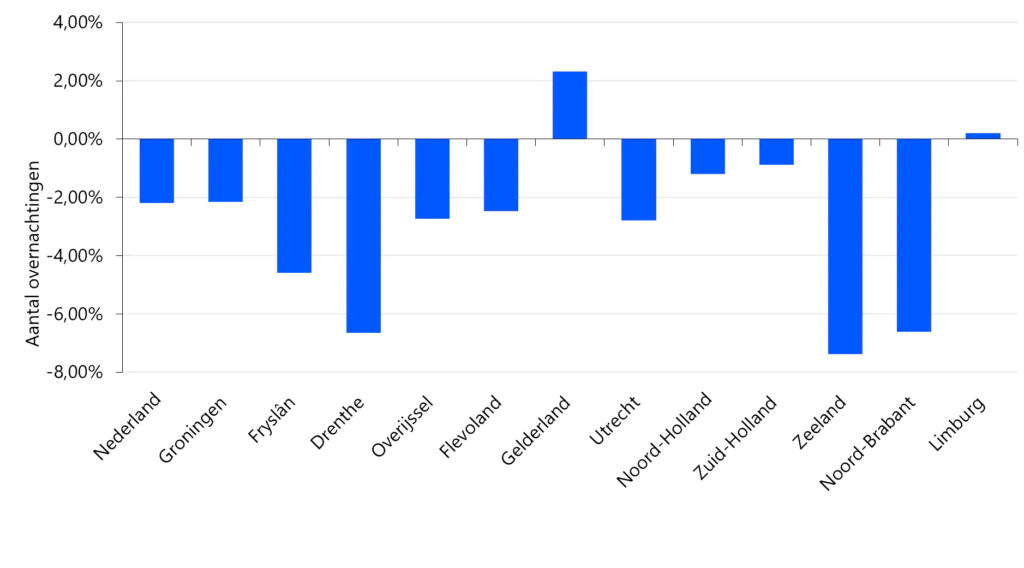

Within the Netherlands, the number of overnight stays is still rising only in Gelderland, by 2.2 per cent. Limburg remains stable. In all other provinces, the number of overnight stays is falling. The decline is most pronounced in Zeeland, at 7.4 per cent. North Brabant and Drenthe follow with declines of 6.6 per cent. In North Holland, the percentage decline in the number of overnight stays is less severe, at 1.2 per cent. Nevertheless, the absolute decline there is significant: 139,000 fewer overnight stays. This means that North Holland, after North Brabant and Zeeland, is among the provinces with the largest decline in terms of numbers.

Figure 3:

Trend in the number of overnight stays up to and including April 2026 compared with 2025.

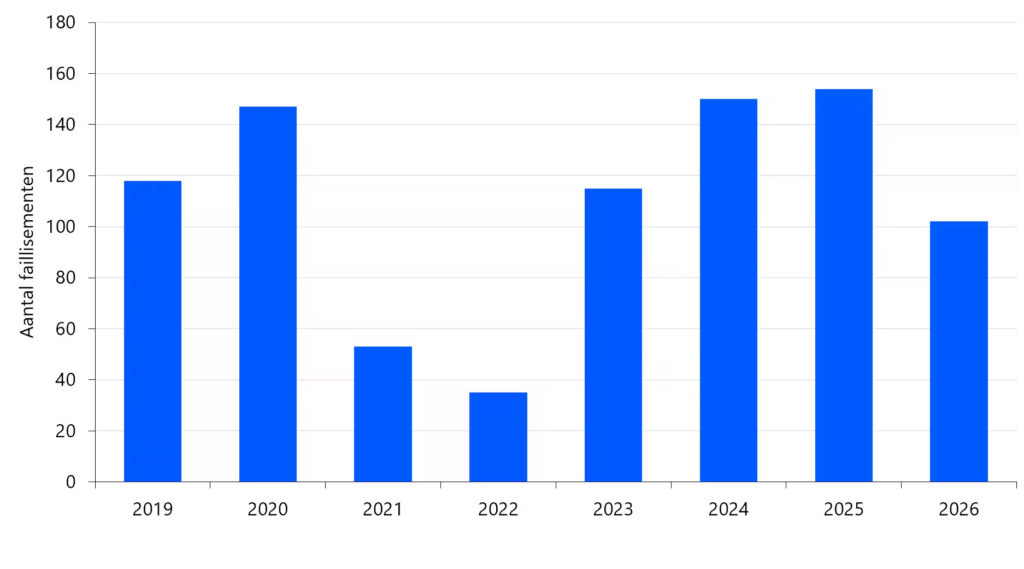

The negative sentiment amongst business owners is not yet leading to an increase in insolvencies in the hospitality sector. A recent business climate survey revealed that 20 per cent of the hospitality sector is struggling with problematic debt and that nearly 40 per cent have seen their profitability decline. Nevertheless, the number of bankruptcies in the hospitality sector fell in the first five months of 2026. The number of bankruptcies remains at a relatively low level and is comparable to that of 2018. The feared surge in bankruptcies following the COVID-19 pandemic therefore appears to have been averted for the time being, despite the challenging circumstances facing the sector.

In contrast to the low number of bankruptcies, the number of business closures remains high. In the first quarter of 2026, the number of closures did fall by 280, to a level comparable to that of 2024. Nevertheless, this is still nearly 700 more liquidations than in the pre-pandemic period.

A decline in consumer confidence often leads to the expectation that consumers will spend less in the hospitality sector. However, this link is less strong than previously thought. A recent analysis by Rabobank shows that general consumer confidence is not a reliable predictor of actual consumer spending. The sub-indicator ‘favourable time for major purchases’ It does, however, provide a more accurate forecast of the consumption of durable goods, such as furniture, tools or clothing.

Although this indicator provides insight into general willingness to spend, its predictive value for spending in the hospitality sector is limited. The indicator mainly relates to large, often deferrable purchases and less to services such as the hospitality sector. Hospitality spending is not only determined by sentiment but is also strongly influenced by price trends. The sharp rise in hospitality prices plays a significant role in this regard. High inflation erodes consumer confidence and reduces the willingness to spend money on non-essential services, such as eating out.

In short: it is not so much a question of whether this is a good time to make major purchases, but rather the combination of price rises and pressure on purchasing power that determines the extent to which consumers adjust their spending on hospitality.